Borrowed Confidence: What FPIs Are Really Betting On

FPIs are rotating out of equities and into government securities.

Imagine a fund manager in Singapore reviewing her India portfolio. She’s been selling Indian equities for two years. Too expensive, too much geopolitical noise, better opportunities in South Korea and Taiwan. That part of her thesis hasn’t changed.

But this month, she bought Indian government bonds. A lot of them.

She’s not alone, and that contradiction is worth understanding.

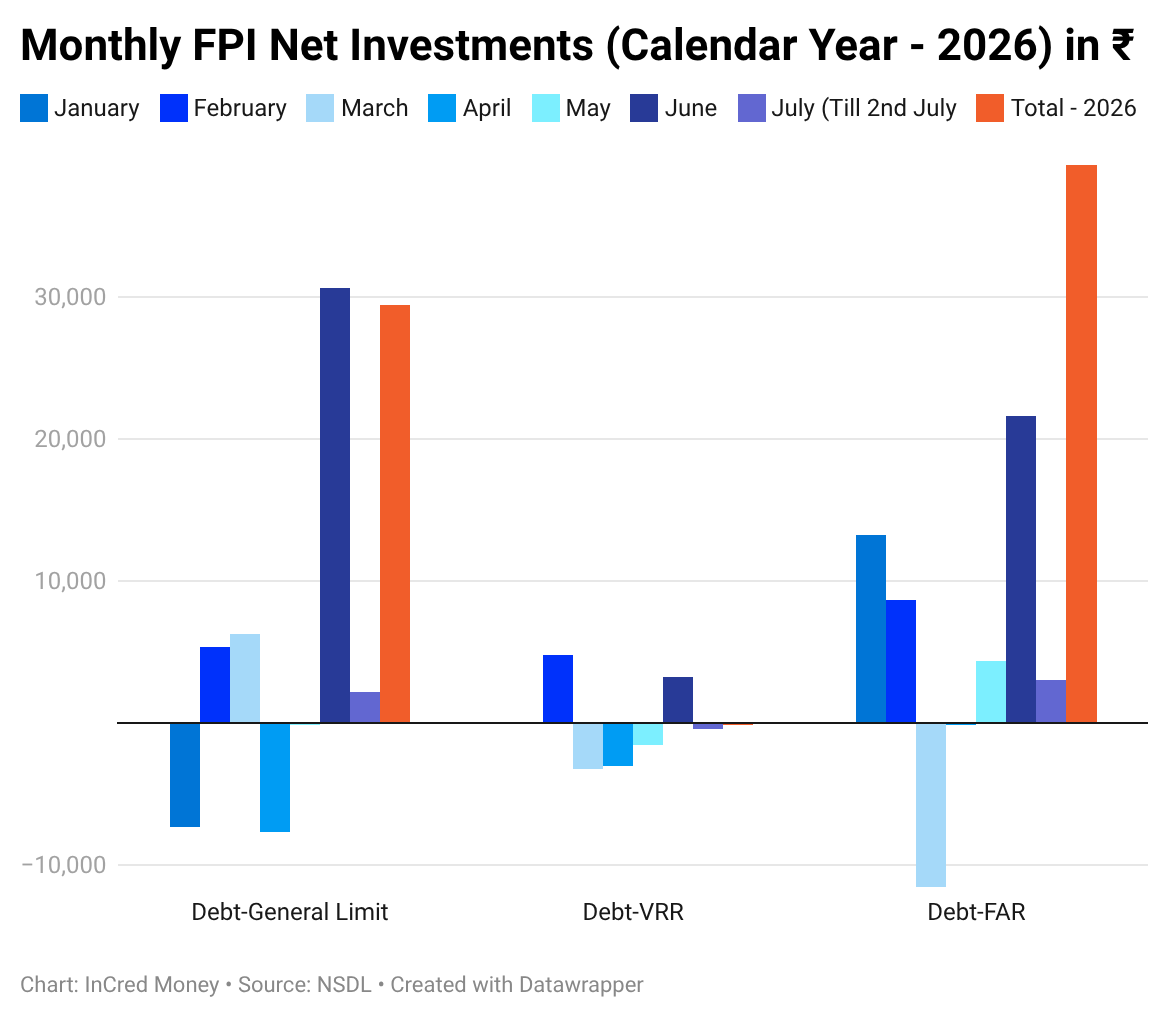

The Numbers That Set Up the Puzzle

In June 2026, FPIs bought a record ₹39,640 crore (~$4.2 billion) worth of Indian government securities, nearly double the previous high of ₹22,005 crore set in August 2024, per CCIL data.

At the same time, FPIs pulled ₹49,340 crore out of Indian equities in June alone. For the full year so far, equity outflows have reached ₹2.74 trillion, one of the steepest sustained exits in recent memory. Total FPI debt inflows for the year now stand at ₹63,784 crore, with the strongest concentration coming through the Fully Accessible Route (FAR) in June and July.

Same investors, same country, opposite behaviour by asset class.

The Yield Story

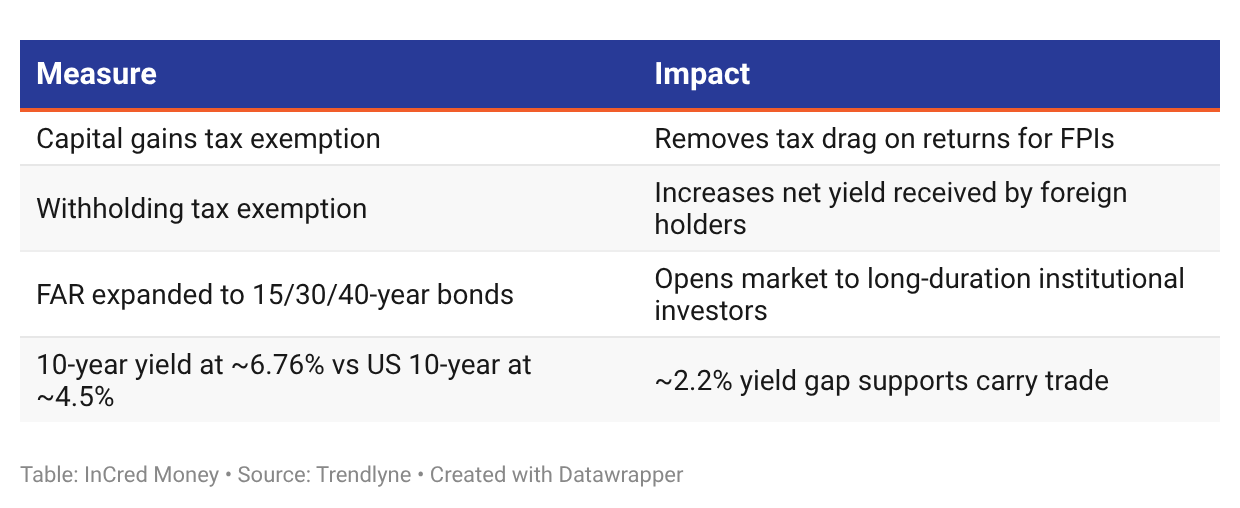

India’s 10-year government bond yield sits near 6.76%, even after easing 20 basis points since recent policy measures were announced. The US 10-year Treasury yields around 4.5%. That gap of roughly 2.2 percentage points means a global fund manager buying Indian G-secs and hedging currency risk still walks away with a meaningfully better return than parking money in Treasuries.

The simple way to think about it: a bond is a promise to pay a fixed amount over a fixed period. If the promised return is higher and the borrower is credible, and Indian government securities are as credible as they get, the math works in India’s favour, especially as the rupee has stabilised after the Iran conflict slide.

The Policy Push That Made It Happen

The June surge didn’t appear from nowhere. The government and RBI announced a coordinated set of measures designed specifically to attract foreign capital into Indian debt:

The FAR expansion is particularly significant. Global pension funds and insurers, who carry long-duration liabilities, finally have long-duration Indian assets to match them with.

Why Equities Are Still Out of Favour

Nifty valuations remain stretched relative to near-term earnings growth

The West Asia conflict, even post-ceasefire, left real scars through higher input costs and squeezed margins

Global capital continues chasing AI-driven markets in the US, Taiwan, and South Korea instead

In short: the fund manager trusts India to pay its debts. She’s less sure Indian companies will grow fast enough to justify current prices.

What This Rotation Actually Does for India

Debt inflows are stickier than equity flows. A fund buying a 10-year G-sec is committing capital for a decade, not a week. This stabilises India’s external account directly, the same account that came under pressure during the Iran conflict when equity exits and a rising import bill pushed reserves down and the rupee toward record lows.

The connection is visible in the data: India’s forex reserves climbed to $672.59 billion in the week ending June 19, up $963 million. The 10-year yield easing 20 basis points since the tax measures landed also lowers the government’s own borrowing cost, real money given the scale of India’s borrowing programme.

There’s a longer-term prize too. Sustained foreign participation strengthens India’s case for inclusion in global bond indices like JPMorgan’s and Bloomberg’s EM benchmarks, which would bring larger, automatic passive flows over time.

The Fragility Underneath

This is not a vote of confidence in India’s growth story. It’s a narrower bet on currency stability, fiscal credibility, and yield, and all three are reversible. If the Fed hikes again under Chair Kevin Warsh, the carry trade math weakens. If the rupee comes under fresh pressure or fiscal slippage widens, the credibility premium narrows.

India did the right things to earn this capital: removed the tax friction, expanded the accessible universe, kept credible institutions. The record June inflow is the result. The question is whether the fundamentals hold long enough for that bet to turn sticky, and whether equities eventually catch up. Until then, the investor who won’t buy Indian stocks is quietly becoming one of India’s most important creditors.

This Week’s Numbers Wrapped Up

India

India’s Fiscal Deficit Widens in April-May

India’s fiscal deficit widened to 9.6% of the full-year FY27 target during April–May, driven by higher spending outpacing revenue.

Capital expenditure spending rose to ₹2.51 lakh crore, signaling the government’s continued commitment to front-loaded infrastructure investments.

United States

US job growth misses expectations in June; unemployment rate falls to 4.2%

The U.S. added just 57,000 jobs in June, well below the 115,000 forecast, while the unemployment rate ticked up to 4.2%.

The data revives concerns about labor market cooling, even as the Federal Reserve under Chair Kevin Warsh remains hawkish on inflation.

Japan

Japanese Yen hits four-decade low against US dollar - why the currency is depreciating

The yen weakened past 162 per dollar, hitting levels last seen in 1986 and keeping markets on high alert for potential Bank of Japan intervention.

This ongoing currency vulnerability and resulting economic pressure stand in sharp contrast to the RBI’s highly confident tone regarding India’s macroeconomic resilience.

What Can You Expect To See Next Week

If you enjoyed reading this newsletter, feel free to share it with your friends and family using the link below!