Ganguly's worst decision ever?

The thinking error that quietly wrecks portfolios

23 March 2003. World Cup Final. Wanderers Stadium, Johannesburg. India vs Australia.

This was the biggest match of my lifetime uptill that point. A strong Indian team in a World Cup final against the best team on the planet.

Sourav Ganguly won the toss and elected to bowl first. He had his logic - the pitch had been damp since morning, the last two World Cup finals had both been won by the chasing team, and Zaheer Khan had been the standout bowler of the tournament. The logic for bowling first was not unreasonable.

What followed was a massacre — Zaheer conceded 15 in the first over, Ricky Ponting made 140 not out, Australia posted 359/2, and India were bowled out for 234.

Critics called it the worst toss decision in World Cup Final History. But had Zaheer bowled out Gilchrist in that first over and the opening stand folded at 40 instead of 105, the exact same decision would have been called sharp, well-read, and brave.

That one over is the thing that separates “a tactical masterstroke” from “a huge mistake” and that gap, between the quality of a decision and the quality of its outcome, has a name: Resulting.

What Is Resulting?

Resulting is a term coined by professional poker player Annie Duke in her book ‘Thinking in Bets’.

The idea is simple: we tend to judge the quality of a decision based purely on whether it worked out i.e. the result, rather than whether the decision itself was sound. A good decision can lead to a bad outcome.

A bad decision can lead to a good outcome. And because outcomes are visible while decision quality is invisible, we keep confusing the two.

The problem is especially sharp in situations involving probability and uncertainty including investing.

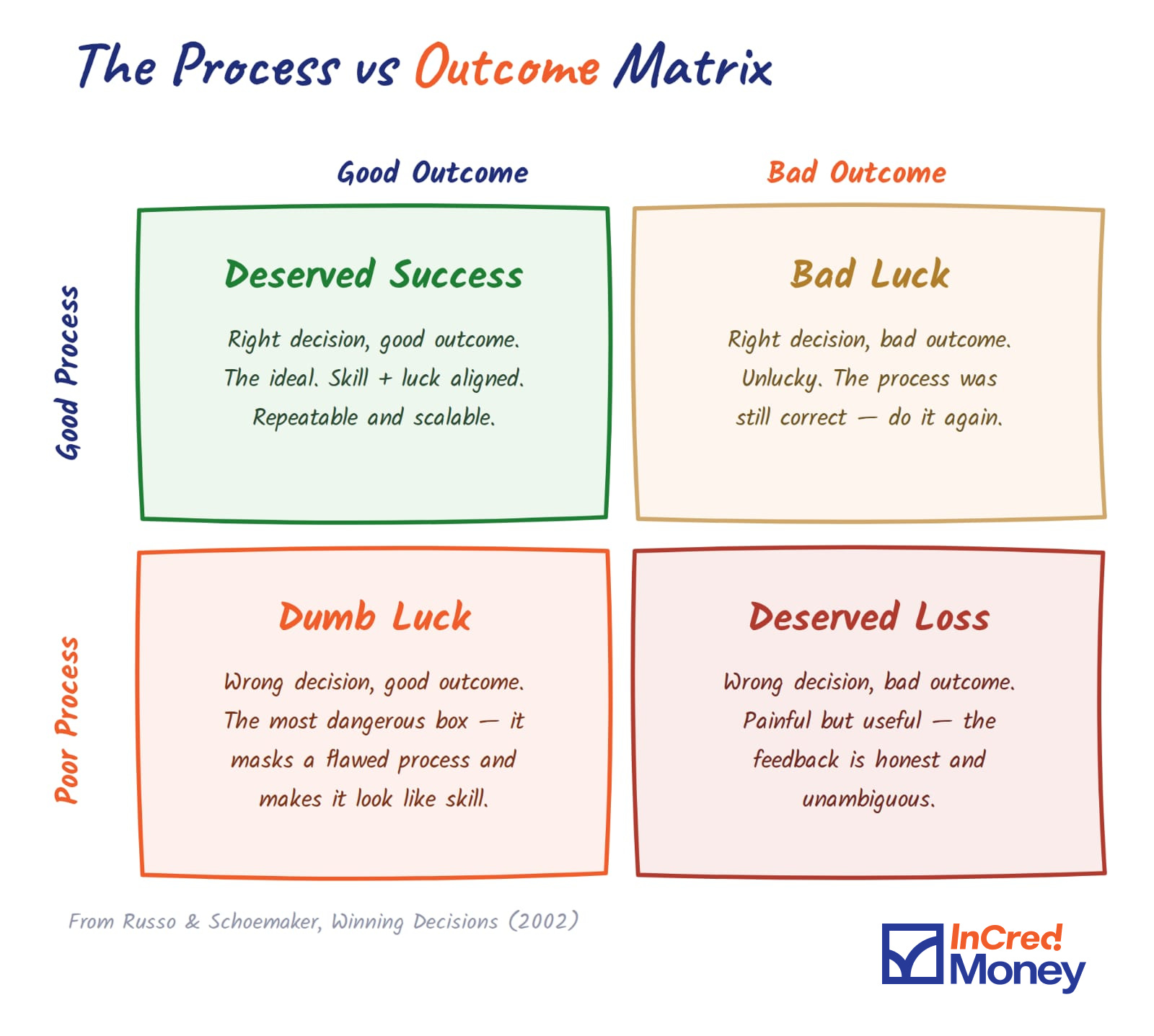

The Four Boxes Every Decision Falls Into

Russo and Schoemaker mapped this in their book Winning Decisions — a simple matrix that plots your decision process against the outcome across four possible combinations. Understanding which box a decision falls into is what separates disciplined thinkers from people who just follow results.

The most dangerous box is bottom-left: poor process, good outcome. It’s dangerous because you get rewarded despite being wrong. That reward tells you to keep doing what you’re doing. You don’t learn anything. You don’t fix anything. And when luck eventually runs out, the whole thing comes apart.

Think of it this way: if you drive drunk and reach home safely, you got lucky. The outcome that day was fine. But keep doing that and surely once you will get into an accident.

Resulting Can Wreck Your Portfolios

The stock market is a probability machine. Almost every investment decision is made under uncertainty — which means good decisions will sometimes lose money, and bad decisions will sometimes make money.

But because we remember outcomes far more vividly than we remember the reasoning behind our decisions, Resulting becomes almost unavoidable.

You might have invested in a hot stock with poor fundamentals in the middle of a raging bull cycle. You had no study on it, but you bought it because it was very popular. You make a lot of money and feel vindicated. But it’s just Dumb luck.

Now you invest in another stock in the same manner and the market turns. You attribute that decision to the market. But in essence, it was a Deserved Loss.

Similarly, a fund manager who has a clearly articulated philosophy and fund management style and a long proven track record might underperform the market in a bull run. That would be more like Bad Luck.

It is possible that investors overlook this fund and invest in a very risky fund just because it showed better returns during the bull run. They skipped understanding the process and focussed only on the results.

How To Actually Avoid Resulting

A few things that could help:

Write down your thesis before you invest: Why are you investing in this? What are the conditions under which this would work, and under which it would not?

Separate outcomes from decisions in your post-mortem: When a trade goes wrong, ask: was the process flawed, or did I just hit an unlikely scenario? If the process was sound, the right response is to do it again.

Be especially sceptical of recent winners: A stock or a fund that has gone up a lot recently is not necessarily a better investment. Don’t invest in something just because their past results were good.

Think in probabilities: The goal is to be right more often than you’re wrong. A 60% probability of being right, applied consistently across many decisions, compounds into something significant over time.

What this could mean for you

Even the very best fall victims to Resulting.

Pep Guardiola, one of the best football managers of all times, once said about the reaction from fans and critics about his tactic of rotating his players for matches, “If I rotate the team and win, I’m a genius. When I rotate, and I lose, people say “why rotate?”.

At the end of the day, you cannot control outcomes. You can only control the process. And in any game involving probability — sports, investing and even business — the only sustainable advantage is consistently making decisions that are on the right side of the odds. That has a higher probability of success than failure.

This does not mean you will always win. It means that over many, many decisions, the quality of your process will show up in your results. Not on any single bet, but across the full body of work.

To sum it up: ‘Luck is not scalable, but process is.’

If you enjoyed this newsletter, feel free to share it with your friends and family using the link below.

Till the next time,

Vijay

CEO - InCred Money

P.S. I share my thoughts on Investing and the Economy regularly. You can follow me here.

Disclaimer: The Logos displayed above belong to the respective company(ies) and do not belong to us and are used for representation purpose only. We do not make warranties as to the quality of the company, disclosures, IPO timelines, valuations or any other matter. It is specifically informed that if you enter into the buy transaction, it shall be on the basis that you have understood and agreed that we and/or our group company/ies shall be the counterparty to the transaction and you shall have no objections to the same at a later date. InCred Money and its representatives are not SEBI-registered analysts or advisors. Any decision to invest or not to invest shall be at your own discretion. Carefully read and understand the risk profile and disclosures of unlisted equities before investing. InCred Money is the brand name of ETA Fintech Private Limited. Pre-IPO shares are unlisted securities, but this should not be interpreted as InCred Money guaranteeing or confirming that an IPO will take place for these shares. The decision to proceed with an IPO is entirely at the discretion of the issuing company, which may choose not to go public. We do not make warranties as to the quality of the company, disclosures, IPO timelines, valuations or any other matter. The information mentioned on the platform is based on publicly available data and to the best of our knowledge, does not constitute insider information. Detailed Disclaimer

Well written the correlation between 2 sports cricket and Trading wah wah .. liked ir

Well-articulated and this says it all - ‘Luck is not scalable, but process is.’