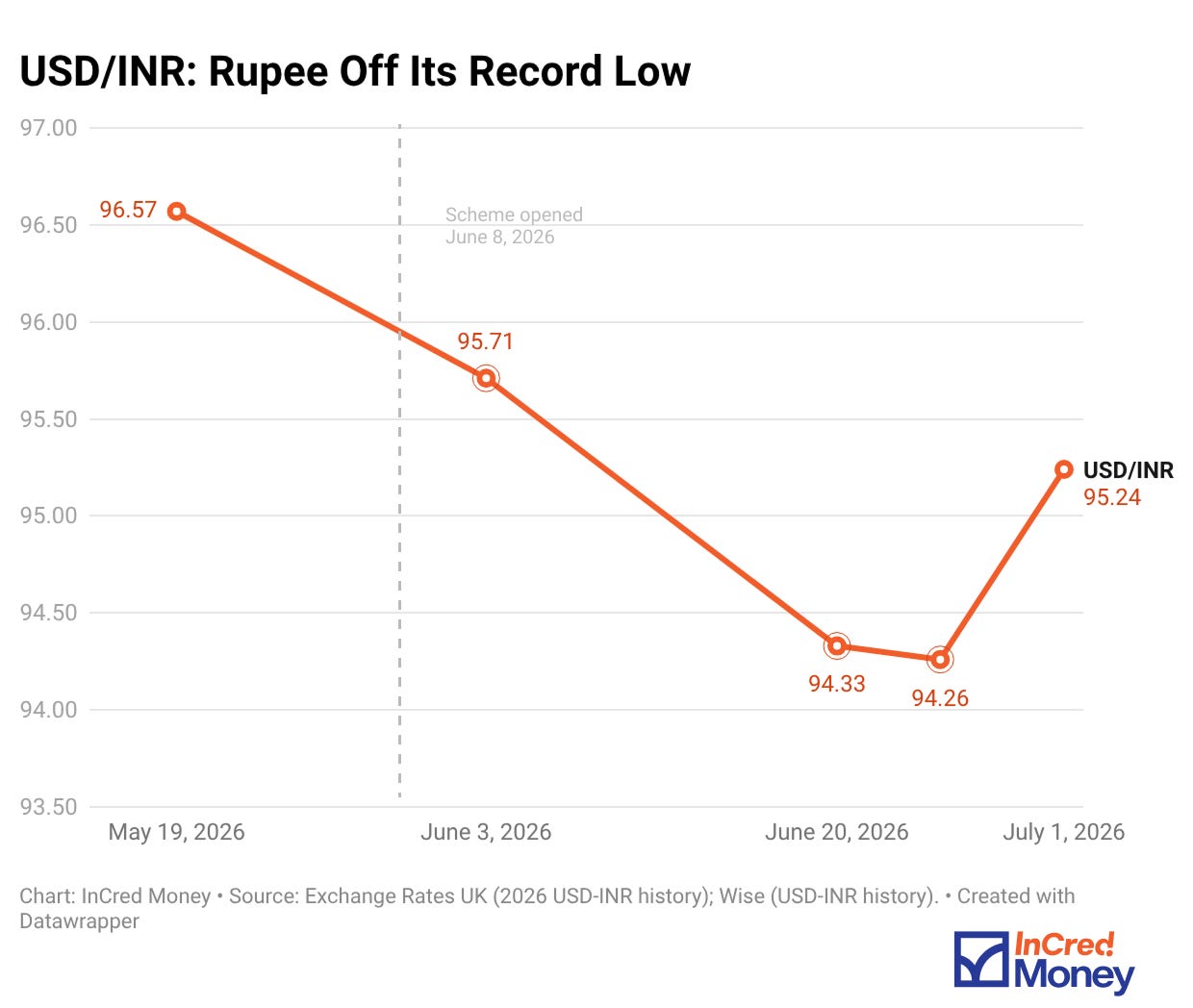

Between March and May this year, the rupee had a rough few months. Tensions in West Asia pushed crude oil past $100 a barrel. Foreign investors pulled out over ₹55,000 crore from Indian stocks in May alone. On 19th May, the rupee slid to a record low of near 96.6 against the dollar.

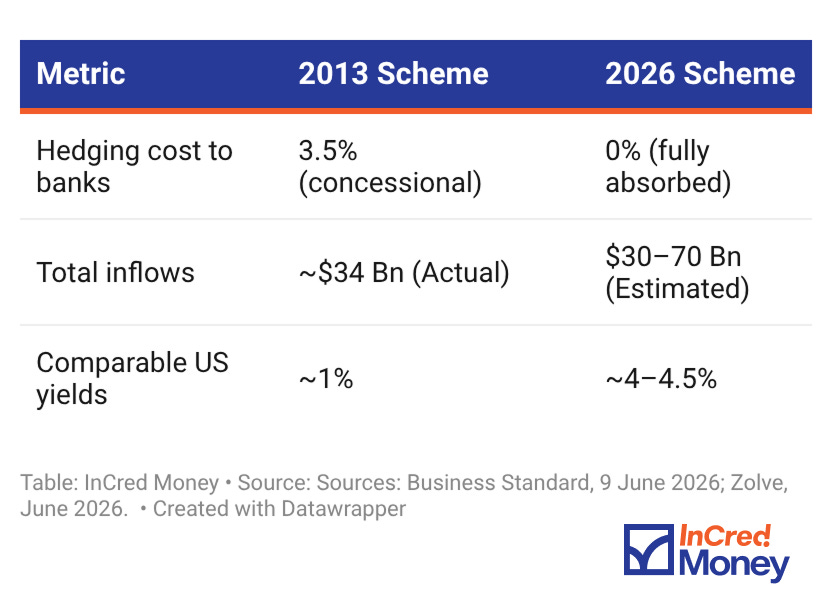

This wasn’t unfamiliar territory for the RBI. It had seen a similar script play out in 2013, during the taper tantrum (when the US Federal Reserve withdrew its monetary stimulus program). Back then, it reached for a specific tool to pull dollars back into the country and steady the rupee. In June this year, facing a similar squeeze, it reached for the same tool again.

This scheme is built exclusively for NRIs. So Resident Indians, can’t invest in this scheme. But if you have family abroad, this is worth telling them about, since it could mean a meaningfully better return on dollars they already hold.

Even if nobody in your circle qualifies, it still helps to understand this. A more stable rupee means cheaper imports and steadier inflation, and both eventually show up in your own monthly budget.

What is This Scheme, Exactly

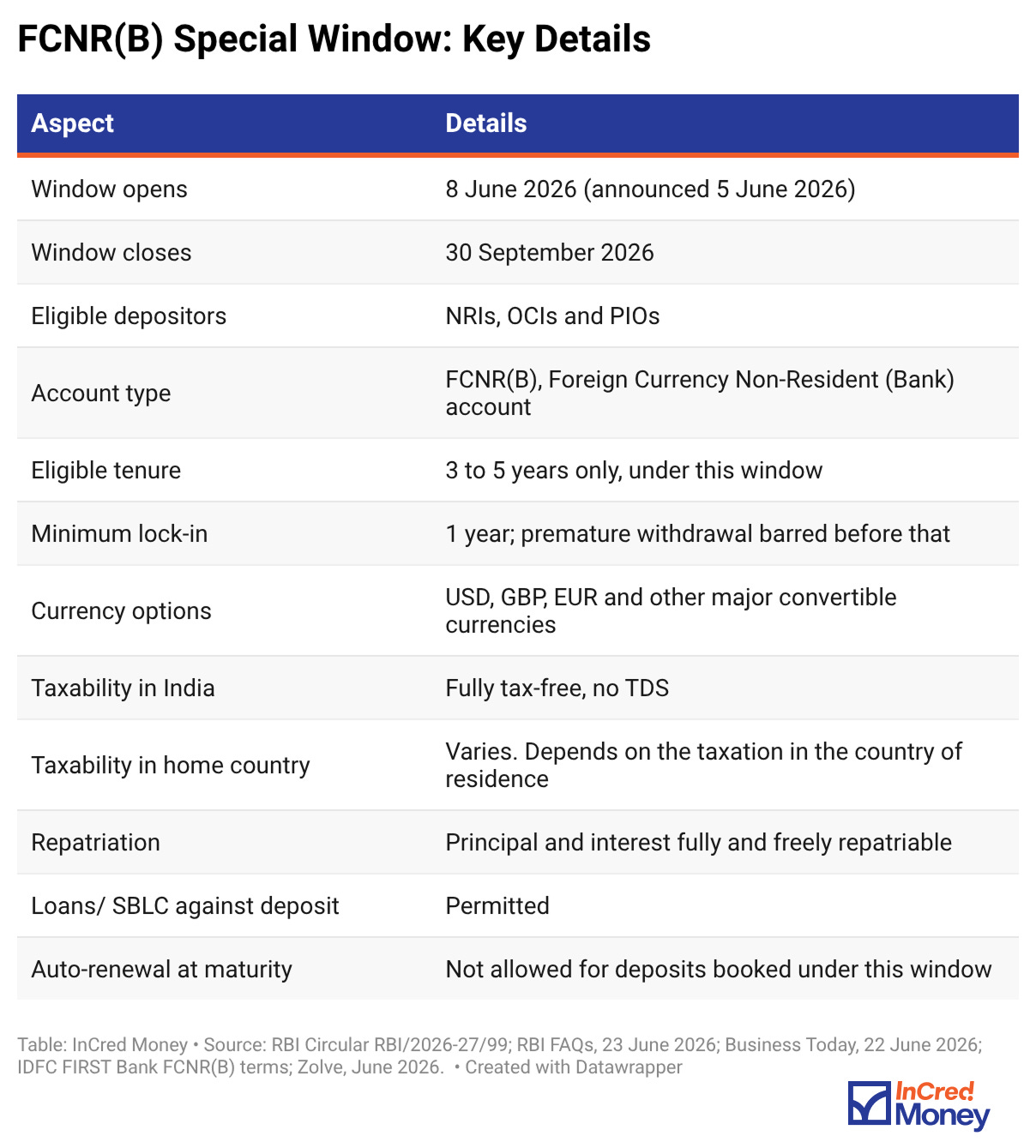

FCNR(B), or Foreign Currency Non-Resident (Bank) account, is a fixed deposit that NRIs can open at an Indian bank in a foreign currency, usually US dollars.

They deposit dollars, earn interest in dollars, and get dollars back at maturity. The rupee doesn’t enter the picture at any stage.

This account has existed for years, but it’s built exclusively for NRIs, OCIs and PIOs. Resident Indians cannot open one, so think of this as something to explain to family abroad rather than act on yourself.

FCNR(B) Key Details

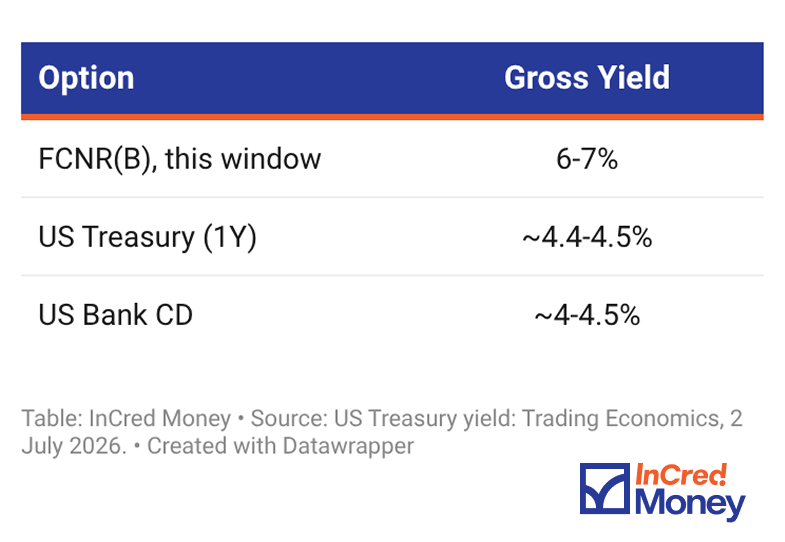

Why This Scheme is Genuinely Attractive For NRIs

Most fixed income options for NRIs involve a trade off somewhere, either a lower interest rate or a currency risk. This scheme is unusual because neither apply here.

Interest is tax-free in India (no TDS in India but it may be taxable in the residence of the NRI), and both principal and interest can be freely repatriated. Since the deposit stays in dollars throughout, there’s no conversion risk either.

It’s also worth comparing this to other dollar debt options. US Treasuries (US Bonds) currently yield close to 4.4-4.5%.

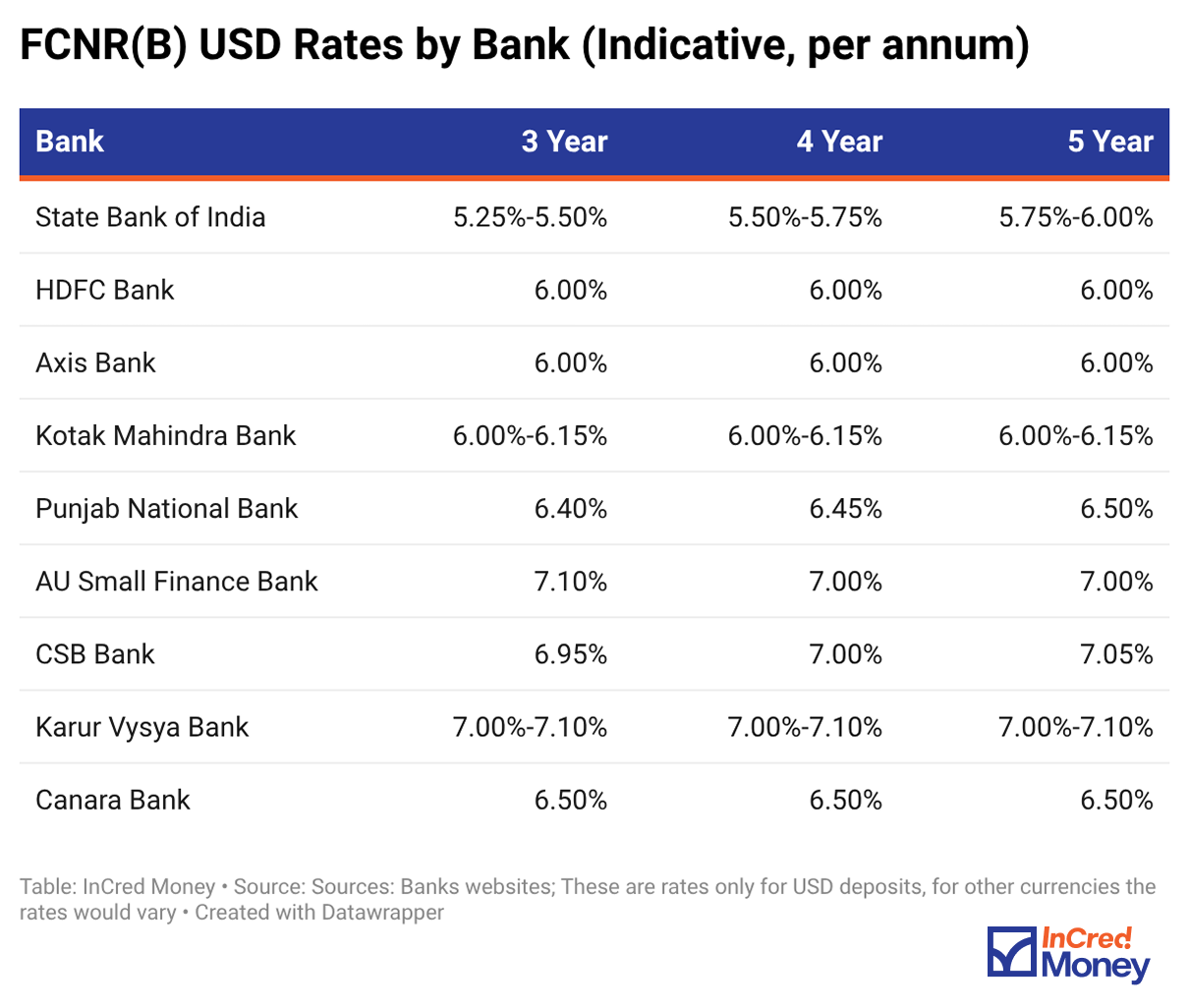

What Rates Are Banks Offering?

How The RBI Made 7% Possible

To see why a 7% dollar deposit is unusual, it helps to know what used to stand in the way.

When a bank takes in a dollar deposit, it usually doesn’t let those dollars sit idle. It converts them to rupees and lends that money out in India, since that’s where the loan demand is.

The catch: the bank has promised to hand back dollars, not rupees, at maturity, three to five years later. If the rupee weakens meanwhile, the bank needs more rupees to buy back the same dollars, and that gap is a real cost.

To protect against this, banks buy a hedge, essentially a contract that locks in today’s exchange rate for a future date. This hedge isn’t free. It typically costs a bank 2 to 3.5% every year, and that cost eats directly into the rate it can offer you.

On 5th June, the RBI announced a plan to remove this cost altogether, for a limited window.

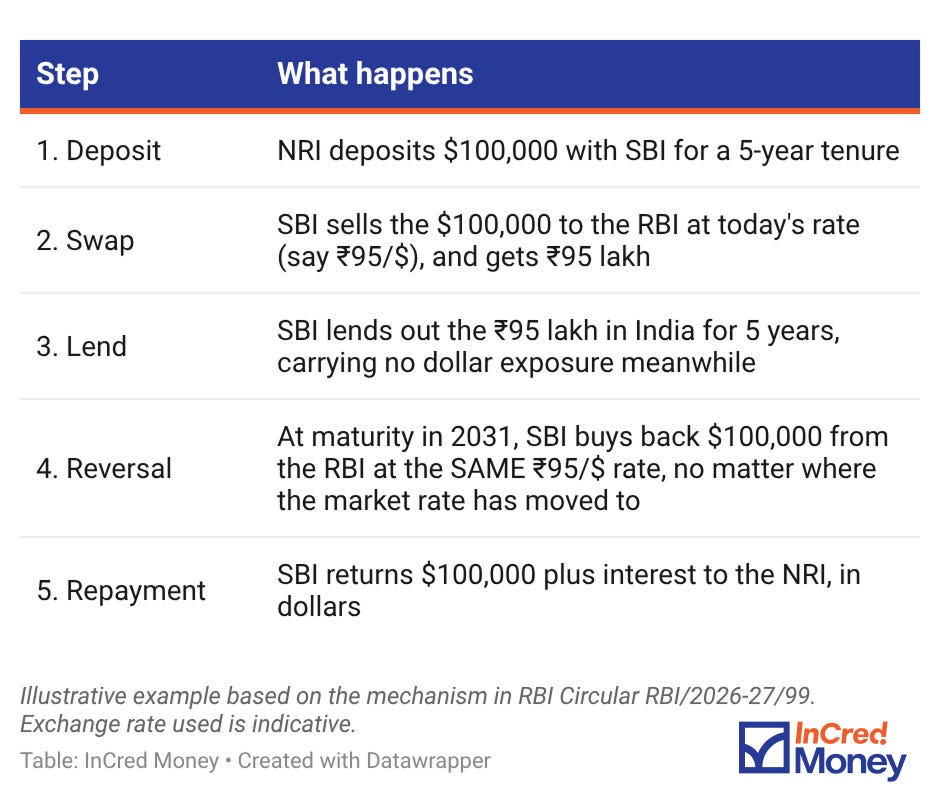

Here’s how the swap works, using a simple example: an NRI in Dubai opens a $100,000 FCNR(B) deposit with SBI for 5 years.

Because the exchange rate is locked at both ends of the swap, the bank carries zero currency risk on this deposit. That saved hedging cost is exactly what lets it offer 6-7% instead of the usual 3.5-4%.

The Leverage Add-On

Some banks, led by SBI, are also offering a leveraged version. Here, the NRI’s deposit becomes collateral for a Standby Letter of Credit, letting them borrow a much larger sum, at 5x to 9x their original deposit, and invest all of it into a fresh FCNR(B) deposit.

This part was murky when the scheme first opened, but the RBI has since cleared it up. The RBI issued FAQs explicitly confirming that Indian banks, including their overseas branches, can extend loans to non-residents and issue SBLCs against these deposits.

At the higher end of leverage, brokerages like Jefferies estimate net returns could climb as high as 17-27% a year, after borrowing costs.

We’ve Seen This Movie Before

This is the RBI’s second time running this play. In 2013, during the taper tantrum, then-Governor Raghuram Rajan opened a similar window, except banks paid a concessional 3.5% for the hedge instead of getting it free.

Has it Actually Moved The Needle?

Three weeks in, some early signs are visible in the data.

None of this proves the scheme alone is responsible, since cooling oil prices and calmer geopolitics are helping too, but the direction fits what a large NRI deposit push would be expected to do. Goldman Sachs estimates the scheme could draw $30-50 billion by the end of 2026, most of it between July and September. As per reports, banks have already collected $7 billion in June.

The Takeaway

The rupee’s stability isn’t just a headline you skim past. It shapes what you pay for imported goods, how much fuel costs, and how sticky inflation stays.

This scheme won’t fix everything, and it has a shorter shelf life than the 2013 version did. But it’s a reminder that when the currency comes under pressure, the RBI has tools, and it isn’t afraid to reach for old ones that have worked before.

If someone in your family abroad is sitting on dollar savings, this could be worth a conversation before 30th September, since that’s when the window shuts.If you enjoyed this newsletter, feel free to share it with your friends and family using the link below.

Till the next time,

Vijay

CEO - InCred Money

P.S. I share my thoughts on Investing and the Economy regularly. You can follow me here.

Disclaimer: The Logos displayed above belong to the respective company(ies) and do not belong to us and are used for representation purpose only. We do not make warranties as to the quality of the company, disclosures, IPO timelines, valuations or any other matter. It is specifically informed that if you enter into the buy transaction, it shall be on the basis that you have understood and agreed that we and/or our group company/ies shall be the counterparty to the transaction and you shall have no objections to the same at a later date. InCred Money and its representatives are not SEBI-registered analysts or advisors. Any decision to invest or not to invest shall be at your own discretion. Carefully read and understand the risk profile and disclosures of unlisted equities before investing. InCred Money is the brand name of ETA Fintech Private Limited. Pre-IPO shares are unlisted securities, but this should not be interpreted as InCred Money guaranteeing or confirming that an IPO will take place for these shares. The decision to proceed with an IPO is entirely at the discretion of the issuing company, which may choose not to go public. We do not make warranties as to the quality of the company, disclosures, IPO timelines, valuations or any other matter. The information mentioned on the platform is based on publicly available data and to the best of our knowledge, does not constitute insider information. Detailed Disclaimer